EMX: Fuller Value Ahead For Serbia Copper-Gold Mine

Royalty buyers in any industry have l-o-n-g timelines for payoffs. They have biblical patience.

Wednesday April 3, 2024 latest: copper's 3.3% daily gain to $4.20 a pound (futures) is the largest one-day rise since September 2018, I see. Silver is rising 4.4% to $27.11. Gold's price: new, high-volume high of $2,325 an ounce. See contracts please. Outpacers Wednesday include Ivanhoe Mines IVN, just out with its copper production figures; First Mining Gold FF; Avino Silver & Gold ASM; Blackrock Silver BRC; many silver-cos; Victoria Gold VGCX. Throw a dart. TRADING NOTES BELOW.+

EMX Royalty | Elemental-Altus Royalties | Metalla Royalty | Zijin Mining | Lundin Mining

I remember, it was 8 years ago (November 2016), I was browsing a gold show at San Francisco‘s Park Central Hotel.

Buyers that day eight years ago saw EMX rising to $3.19 in the next 4 1/2 years; EMX along with many (but not all) metals equities (stocks).

Robo-trend analysis: EMX appears to be in a strong bullish trend. Its 200-day moving average is upwards sloping and the MACD histogram is above 0. **

EMX shares are in a dump again since May 2021. Many royalty companies are.

Plus income from its Leeville net-smelter return (royalty) in Nevada via a Barrick-Newmont Mining partnership; income from its Balya Turkey zinc-lead-silver royalty; its Gold Bar royalty in Turkey via McEwen Mining MUX. I could go on.

Advanced royalty projects and exploration projects on the list number past 100 and are almost everywhere on the map except for Africa. See lists here please.

When principals call me, and not the other way around, and there is no news release attached, just EMX’s year-ending MDA management discussion, so how can I say this? Dave Cole knows his stock market betas; he is a practiced investor for himself and for EMX. I’d say he has a 70% success rate with me when he drums his fingers on the dirt-cheap table.

Straight off, Dave says about the debt that keeps coming up with some shareholders: “EMX used said debt to buy Lundin Mining’s Caserones NSR, which was a great investment. EMX has ample cash flow to manage said debt forth going.”

“EMX (has) a range of royalties within its portfolio. We expect it to see meaningful growth in revenues and cash flow, with several assets poised to enter production in the intermediate term.” Heiko Ihle at HC Wainwright

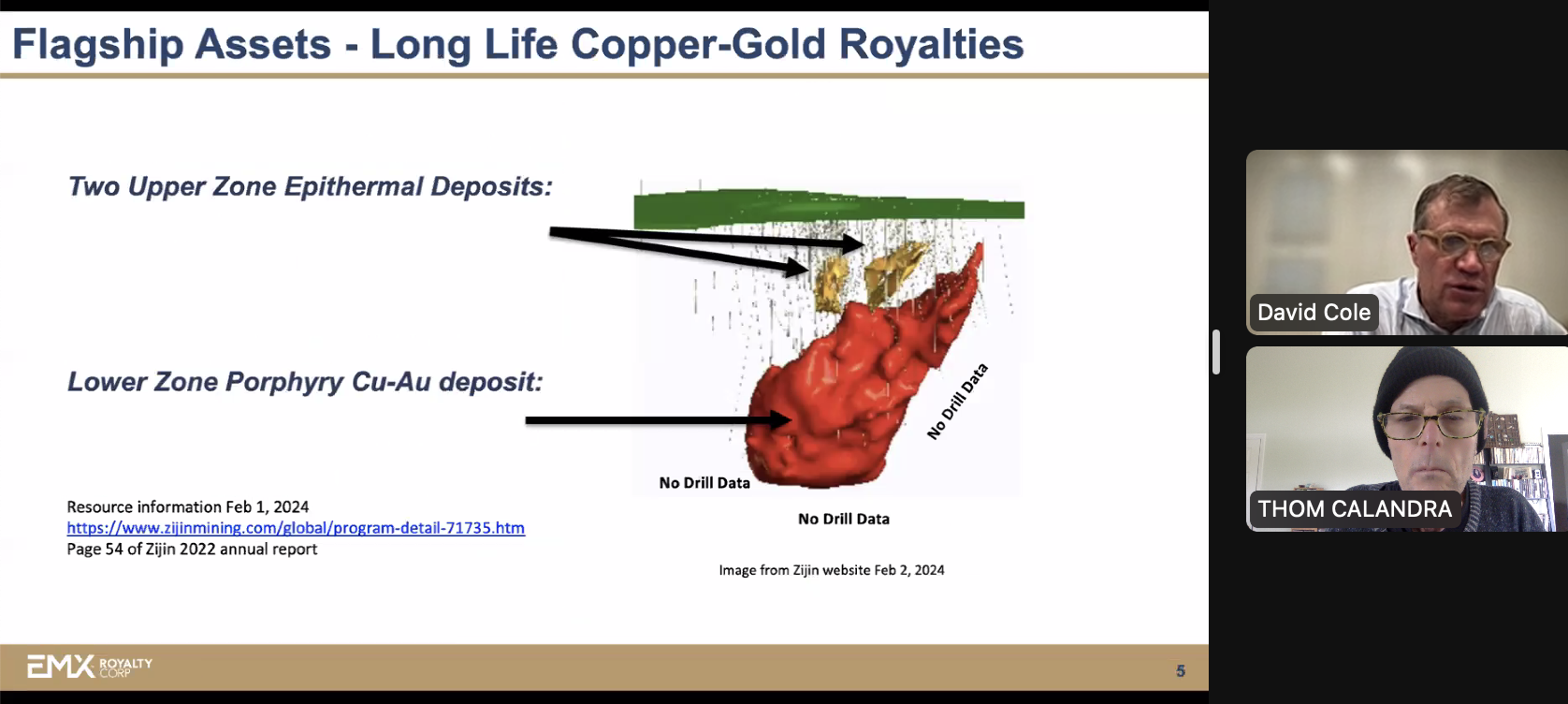

— Please look at pages 8, 9 & 10 this deck: https://emxroyalty.com/corporate-presentation/. Mineralization extends downward and to the left onto EMX’s 2% (gold & silver)/1% (copper & all other metals) royalty footprint. As for the exploration, Google Earth shows 7 headframes at Timok (Cukaru Peki). Plus two so-called declines that will be used to haul ore from the new underground areas. This is from Zijin’s corporate site: Projects-Zijin Mining Group.

— Apply the 0.3625% NSR to those numbers, the royalty revenues’ life of mine, assuming 100% recoveries at today’s prices, with no increase in the copper or gold price and no exploration upside, would come to as much as $729 million. Pragmatically, why not slash that for now, what with the varying costs of recovery scenarios, the smelting into cathode material, the energy costs, to $500 million of net smelter returns. That is at current copper, gold and silver metals prices.

Naturally, if the commodities cycle for higher metals prices streaks onward, and-or Zijin benefits from further ore discovery at depth and laterally, the numbers grow. These envelope estimates also shrink with collapsed caves, a global slowdown or some investors’ nagging China shingles.

Still, Dave and his board members reference “what Gold Strike Mine in Nevada is to Franco Nevada.” FNV at $24 billion billion is the most successful mining roy-co in the world.

TCRs, I give you the boilerplate in the income statement for year-end 2023: cash flow of $7 million for the year; revenue and other income of $26.6 million. I think barreling cash flows in the next 3 years will make EMX a takeover candidate … and-or groom it for an expanded Franco-Nevada project search partnership.

I hope this is not over-burden here, folks: “Zijin is the best counterparty to have because they are the best at getting metal out of the ground and have access to vast amounts of capital,” Dave Cole says. “If Freeport McMoRan FCX still had that thing they would still be twiddling their thumbs.”

* I also am heads over heels into Elemental-Altus Royalties (Africa, Egypt) ELE ELEMF and traded in London and in Canada and U.S.

I admire as well what Brett Heath has done to get his Metalla Royalty & Streaming MTA on NYSE to the dividending stage and a $270 million market value, and I will chat with Brett this week. Metalla in December completed its purchase of Nova Royalty’s 23 NSRs, all of them copper.

I add that MTA is just today-Wednesday April 3, 2024, exchanging hands above its 200-day moving average. The stock is rising 8.8%. Technical chart analysts use that moving-average rigger for momentum — up and down.

** Robo-trend analysis: MTA is showing strength within a longer-term bearish trend. Its MACD is above the signal line and shares are presently 4.1% above the 200-day moving average. That moving average is declining, implying that caution is still warranted. A LOOK AT METALLA (and roy-cos generally) COMING THIS WEEKEND.

+ Trading Notes [updated Thursday April 4]: TCRs, as you know, I own ELE but not MTA. Other ownership notes above please.

Also, I look in this first week of April 2024 copper-gold-silver rally to pare one or two holdings (as of April 4, 2024) to pay property taxes and to diversify and-or fortify existing stakes, namely Banyan Gold BYN; EMX Royalty; Elemental-Altus Royalties ELE. These will be approximately $1,400 of accelerating Ivanhoe Electric IE, of which we own approximately $13,000 USD worth, all profitably since first purchase four months ago; and $750 of (also) accelerating uranium-co enCore Energy EU. I will be placing these orders after this report reaches our TCRs.

** Robotics for trend analysis via Charles Schwab & Co.

— Thom Calandra

Thom Calandra is a writer and an investor. Research and material are meant as editorial opinion. He is not a professional investment adviser. Please do not consider his reporting as a recommendation to buy or sell securities.