That next leg up of an interest-rate and Israel-Hamas driven gold price rally has gold reaching toward $2,000 an ounce. [On Friday October 20, 2023, gold futures surpassed $2k.

Few explorer stocks are benefiting. Ditto producers, roy-cos. The 1-year U.S. Treasury yield is flirting with 16-year highs. [See chart please.]

Executives who run small metals and uranium explorers-producers often will ping me with their thinking behind a “promote,” or a drill result, a new-co, or even a “special situation” regarding their stocks’ low-grade values (this year, anyway).

Sometimes, their squibs, or their longer missives, on the phone, in email and on WhatsApp, are worthy; sometimes, they are four-fifths hooey. Entire report here please.

Example — this morning from Craig Parry, successful Aussie uranium-co founder who specializes in Canada’s Athabasca Basin:

Cosa Resources (a new-co — COSA COSAF $10 million value): “It’s my ex-Isoenergy/Denison/NexGen team. All stars. Take a look.” Craig, a geologist and financier. and his Inventa Capital are Cosa investors and he is a Cosa advisor. See bio please.

Such squibs, or longer conversations, insert a company name or a trend or possible investment into our The Calandra Report/TCR crowded roster of wanna-be miners (or anything, for that matter).

Otherwise, I likely would not become aware of a “new-co,” or new-property, or new-assay, or new-exec, or a fresh scandal, until the thing has doubled or tripled or fallen likewise — from a measly, foundling value or from an inflated price.

[Note: I own no shares of COSA, not yet, anyway; I am on the lookout for ground-floor uranium explorers, as we all are. My ownership of small U-companies consists of CanAlaska Uranium CVV CVVUF; Laramide Resources LAM LMRXF; and Encore Energy EU step-brother/Wyoming explorer Nuclear Fuels NF URVNF. On my wait list to purchase is Skyharbour Resources SYH SYHBF.]

Craig, a prosperous wheeler-dealer active in Vancouver, B.C., has Wes Short, formerly of uranium explorer Isoenergy ISO, as a marketing executive and director at COSA. The CEO-geo he is backing, Keith Bodnarchuk, spent time at Athabasca Basin’s Denison DNN.

Parry’s squib to me prompted interest when we distributed this report the other day.

Hubert Bouchard, a Québec mining executive, said “the following got me intrigued: team background, strategic position of what appears to be their core asset, market cap vs. treasury and the momentum in the uranium market nowadays.”

COSA has seven properties, all trending northeast in the Athabasca Basin. See map please.

A separate comment from a New Mexico/Australia-focused uranium executive I trust said, “It but looks well structured and I would not bet against Craig Parry. Discoveries of any kind are rare though and Athabasca particularly high risk. It is for brave hearts and deep pockets.”

COSA, by the way, does not pay me and is not a subscriber to The Calandra Report/TCR. I am interested because of the cheap factor: $10 million market cap with cash and a tiny share count (for now, anyway).

Yet another uranium executive, whose Texas-slung company will be producing concentrate before year-end, says uranium investing in Athabasca Basin, which has a reputation for extreme high-grade ore in challenging mining conditions, is for short-ranged speculators.

“None of them will make it to production in our lifetime,” he says. “Any of them hit a big intercept they fly and then fall back to earth if no more great holes in rapid succession. With permitting timelines so absurd in Canada (esp. for uranium) they still won’t see production within 10 years.”

This week: Outpacer for The Calandra Report/TCR -- DHT Maritime Holdings DHT; shares above $11. This month, TCRs, we are seeing a whiplash rise in spot cargo rates for crude and LIQUID nat-gas ($35,000 to $60,000 range).

NexGen Energy NXE is probably the best one to watch regarding when the now-$2.3 billion explorer-developer will start pulling ore from ‘basement’ deposits in the southern Athabasca Basin in Saskatchewan Province.

The executive quoted above notes thinks the timeline will be “end of decade … and they have been at it for a decade already.” NexGen says sooner.

“Then there is the huge CAPEX for anything in the basin.”

For investors? “Sort of like going to Vegas without the free drinks. Can still be fun, just remember to sell when they take off.” NexGen also owns 51% of Isoenergy ISO ISENF.

Sometimes, what execs tell me is meant just for me, sometimes for our audience here at The Calandra Report/TCR and sometimes, for the world — just personalized and then replicated in a mass ‘send’ or via multiple calls.

Rarely, the dope they relate is privileged and should be quarantined; i.e., insider dope. In that case, I tread carefully.

OUR 'TRUSTED' ROSTER* regarding all things uranium:

Marc Henderson at Laramide; Daniel Major at GoviEx

Uranium GXU; Bill Sheriff at enCore Energy; Jordan

Trimble at Skyharbour Resources SYHB; Cory Belyk

at CanAlaska Uranium; Craig Parry of Isoenergy, COSA

Resources.

East vs. West

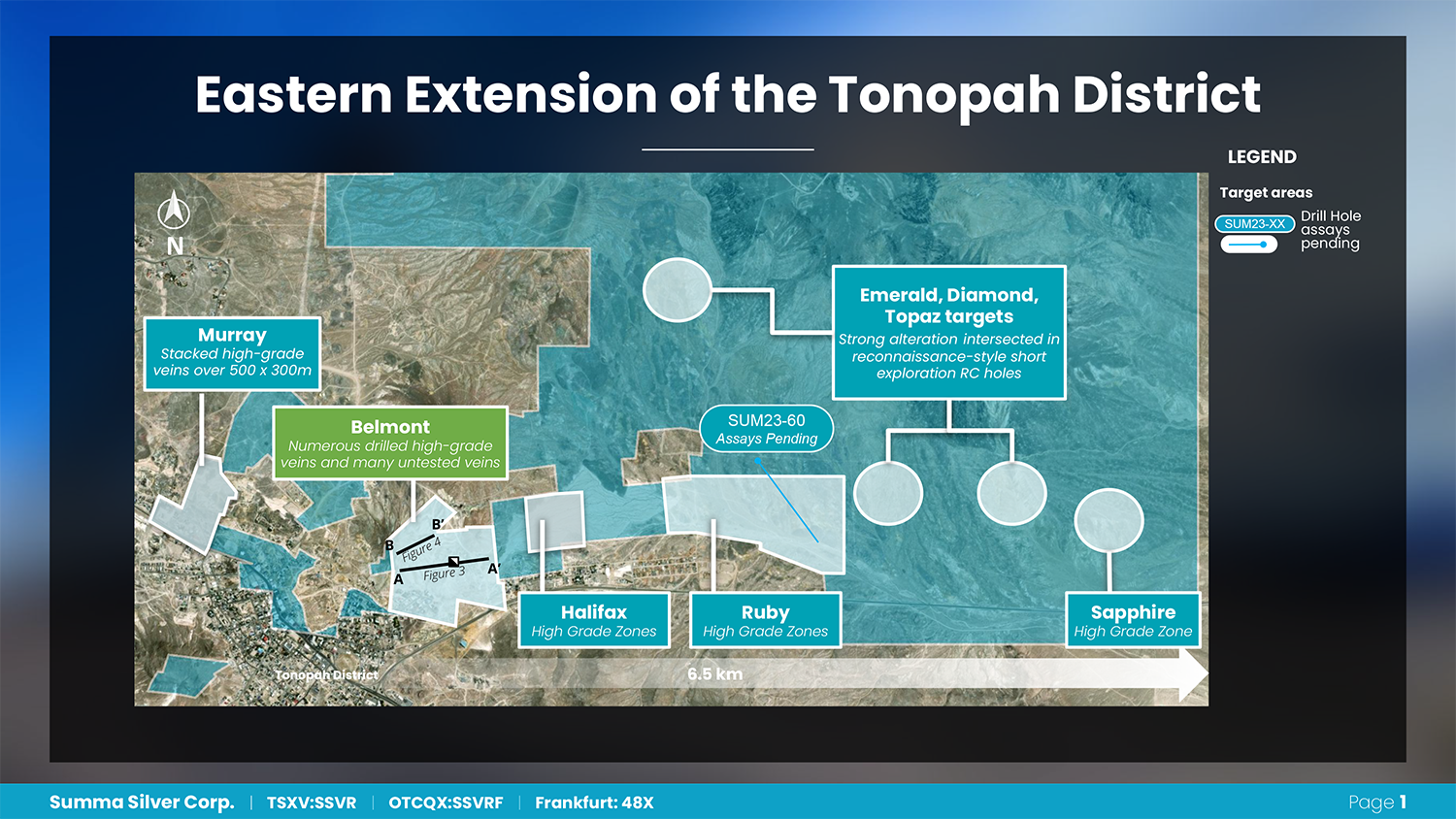

The other day, Galen McNamara at Summa Silver SSVR SSVRF gave me context for a data-driven press release about its (Howard) Hughes Project’s old Belmont Mine on the eastern side of the Tonopah Mining District in Nevada.

“Big resource from our neighbor (Blackrock Silver BRC) this week. I’ve really been thinking about what’s left in the district in total,” Galen, a geo-CEO, says.

I have been to his project twice, and to other Tonopah projects, namely West Vault Mining‘s Hasbrouck gold spread, three times. [I own WVM WVMDF shares, and they are not yet in the hole.]

“Our drilling in/around the same area returned high grades. If there is 100 million silver-equivalent ounces equivalent remaining in the western half of the (Tonopah) district and its extension, what’s left remaining district wide? That’s what I think about,” he says.

“Especially with our holes hitting mineralization well east of the district this past summer at Hughes.”

TCRs, the special situation missive I got the other day from Luke Alexander at Newcore Resources (Ghana) NCAU NCAUF is one where I put money where my laptop is. I already tagged TCRs regarding that “redemption” idea — here please.

“Now is a good time to take another look at Newcore,” he was saying. “We saw significant volume (about a week ago) as a result of a tax-loss seller capitulating, and we believe that tax0-loss selling in general has put undue pressure on our stock recently.”

Newcore “gold” valuation: the stock sells for approx. $6/oz USD, which is 0.10x the 2021 net present value of the project as determined in an econ-stufy in 2021. “I believe,” says Luke, “that as a result our valuation is unreasonably low and hence this presents a value buying opportunity. I last bought stock at $0.15 CAD, so putting my money where my mouth is.”

I like Ghana a lot for many reasons — see previous 11 years reporting regarding Xtra-Gold Resources XTG XTGRF. CEO and country manager James Longshore (and I) and a co-founder of XTG will be in Zurich Nov. 10-13 at Precious Metals Summit. [XTG is our second longest-held resources investment.]

*Trusted roster -- as in, none of these execs have burned me or our The Calandra Report/TCR audience. Plus, they have the uranium dynamics dead to rights.

— Thom Calandra

PayPal $179 Yearly: Recurring The Calandra Report

Thom Calandra is a writer and an investor. Research and material are meant as editorial opinion. He is not a professional investment adviser. Please do not consider his reporting as a recommendation to buy or sell securities.