TCRs, these are “spec-sits.” (Speculative and special situations.)

Special situations in natural resources can become extra special in this current, long-awaited up-cycle for most metals and, finally, for their associated mining-co shares. Led by a swift catch-up from silver.

— CEF is the former Central Fund and now Sprott’s $5.4 billion Gold Silver Physical Trust, which I have owned for decades. The fund gets its stock market oomph from both precious metals; when silver is catching up to gold, as it is now, CEF could see it trim its usual discount to net asset value.

That does not happen often. If and when it does, the fund’s price could trade at par with NAV … or if small investors rush to gold (and silver) in a panic, push the price to a premium of NAV. Regardless, the numbers look fine: 1,3 million ounces of real gold in at least two Canada repositories; 55 million of silver.

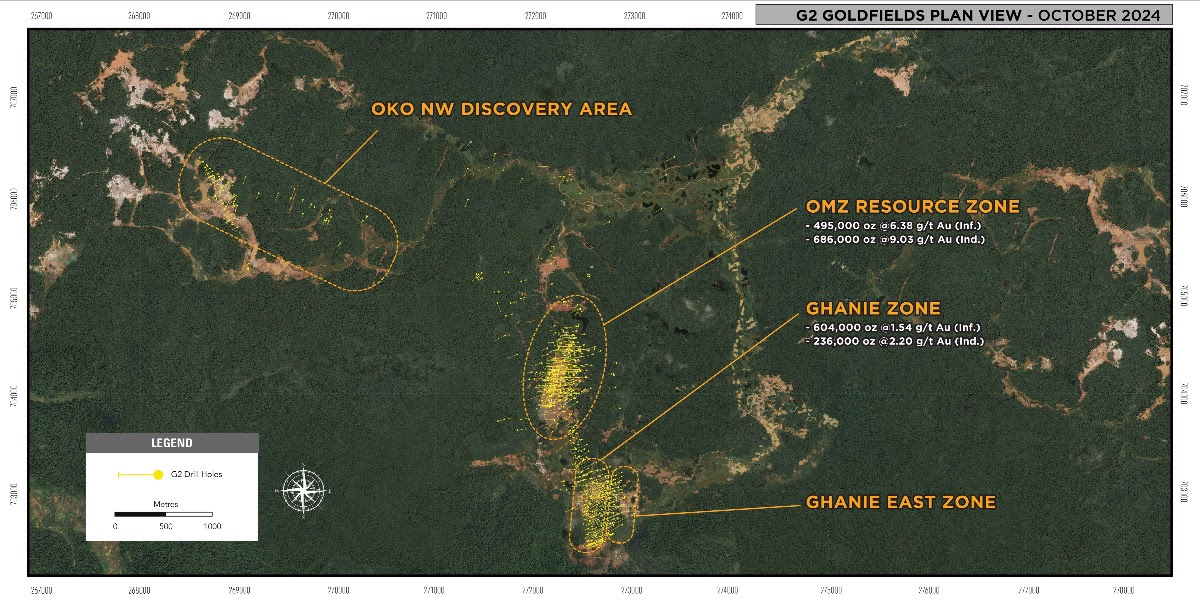

G2 Goldfields

Ghanie Zone: Many diamond drill holes, many ‘pierce points’ — click for larger image.

— GTWO GUYGF: I must tag G2, the Guyana operator of a 58,000-acre OKO-Aremu gold project. G2 has 5 rigs operating at the project. No excuses for not tracking G2 more faithfully; GTWO shares are probably one of the most consistent gainers of the past year, two years and three years. See chart.

The company, helmed by a geo-CEO, Dan Noone, and a well known gold investor, Pat Sheridan, drills almost incessantly: in one zone, Ghanie, almost 200 drill holes (and 400 ‘pierce points’) to the south of the OKO trend.

Maybe this explains the G2 market-cap progression to approx. $400 million plus USD? See image.

AngloGold Ashanti AU owns 15% of GTWO shares in an investment made 10 months ago. Plus: at last look, G2 holds $49 million cash on the books and a few more assays pending. Maybe those are additional drivers?

Pat Sheridan, based in London and executive chairman, is well known in Guyana, a gung-ho minerals nation with plenty of 5-gram-plus gold, if you can get to it. Guyana, where I have seen projects three times, is on South America’s northern Atlantic Ocean coast … and getting more outside capital these days for offshore oil-gas deposits than for its high-grade gold (and copper).

G2 just went partners with a Guyana familyon 30,000 additional acres of possible gold deposits. The area, known as OKO-Aremu gold district, holds a compliant 7.8 million gold ounces. See release.

We’ll try to keep G2 and its 2 million-ounce resource (indicated and inferred categories, with some tonnage as much as 9 grams gold) in the mix.

I do not own the shares but once did and made a small profit that would have been much greater, as much as a 3x, with p-a-t-i-e-n-c-e.

* Thom-Note: TCRs, I will be targeting no more than one report a week — this after (believe it) requests from subscribers to reduce the number. I am always available via email. I also will be stopping new subscribers to the reports as I try in the next several months to “wind down” the business, but not my services to you. Let me work it out. Thank you!

— Silver: A worthy piece by long-time silver/solar panel advocate Simon Catt in London. Good timing as silver prices and dormant silver explorers appear to be waking up — rising dramatically as measured by small-miner gauges.

As you read this, Simon (‘CatCalls’) of Arlington Group, a small investment bank, today tells me his favorite low-priced silver-co is Discovery Silver (DSV). See below for two other speculative, ignored silver-cos.

Via Simon Catt in London

“Discovery‘s largest undeveloped silver reserve n the world at the Cordero open pit in Mexico is at 300 million ounces and US$2 billion NPV at $30 silver, Tier one management, Eric Sprott owns 26% and Jupiter at 14%; I think it is the special one,” Simon says.

Simon notes that in October 2024, gold and silver led other commodities with 30% annual gains.In 2023, industrial demand for silver, led by solar panels, electronics, and electric vehicles, was 54% of total demand, according to The Silver Institute.

“Silver is a relatively small market with approximately $33 billion of annual demand versus $425 billion for gold. If China were to divert 10% of gold demand to silver, that would equal one quarter of the entire annual silver demand.” — Simon Catt

— ** RIDGELINE MINERALS RDG RDGMF: I forgot to tag Nevada’s Ridgeline Minerals for silver in this original report. The shares are surging this week and it is long overdue.

As SF fund manager Matt Geiger reminds me, “Remember that Selena, which was recently optioned to South32 with attractive deal terms, is a sliver-dominant asset. Should see first South32-funded drill program in 2025.”

How do I forget? (Let me count the ways these days.)

Matt of MJG Capital and I were at Selena with the company; and I bought more RDGMF last week. Ridgeline and CEO Chad Peters and team have at least three working exploration projects in Nevada, including a venture with Nevada Gold Mines (Newmont & Barrick). Boilerplate here.

RDG shares are waking up with the silver price gains this week. No news this week that I am aware of.

So are other small, non-producing explorers with little-known gold-silver deposits and-or property aggregators that are seen as below fair value as measured against NAVs of peers.

View from West Vault Mining’s Hasbrouck Peak 25 Minutes’ Drive East of Tonopah, Nevada

One of them is West Vault Mining WVM WVMDF, rising 30% with increasing volumes the past 4 trading sessions (through Wednesday Oct. 23, has long declared it will sit on its resource compliant, shovel-ready gold deposits in Nevada’s Tonopah Mining District.

That is, spend as little money as possible — waiting for a buyer with a fair price offer.

“We’re not aware of any developments,” CEO Sandy McVey tells me this week. An interview with a Boston investment manager this week, one with beaucoup X (Twitter) followers, likely helped, I think. See: West Vault Mining video.

— Two obscure silver-cos: for those who like their extreme-risk choices at the far end of the spectrum — Nubian Resources NBR and Honey Badger Silver TUF.

I own neither. A few CEOs, two geologists and one banker have been asking me (for a l-o-o-o-n-g time) to look at the tiny-cos.

Nubian, market value a miniscule $4 million, is all over the map: Peru, Australia, United States.

“This Nubian is a definite sleeper and we will be reactivating it very soon. We are doing a rebrand first (name change etc) but at +$30/oz silver this must be one of the more undervalued names out there,” says Marc Henderson of Laramide Resources LAM, a uranium-co.

Marc is chairman of Nubian. He has yet in several years to lead me astray.

“It’s been hard (as I know you know) to find sponsorship for microcaps but the precious metals are finally starting to find a new audience and this is a name that should perform well when that happens. We own a bunch of other pretty decent assets and the insiders own a lot,” he says.

Honey Badger Silver TUF is exploring and compiling, or aggregating, properties in Yukon, Northwest Territories and Nunavut. Chad Williams, a banker who started Red Cloud Financial in Toronto, chairs Honey Badger. More here.

Chad, who has a large audience at several venues, has been on me for three years about Honey Badger. He owns 27% of the company, which advocates “aggregating” silver assets and waiting for silver’s price to reach $100 an ounce.

Chad’s appointed Honey Badger CEO is a longtime geologist, Dorian L. Nicol — see here in a video.

I have not taken the time to familiarize myself with Honey Badger’s assets. Right now, with precious metals (gold, platinum, supercharged silver) staging what looks like a cyclical rally, I am swamped with ‘look-at-us’ pleas from ignored mini-explorers.

Sprott Physical Gold Silver Trust Snapshot (Click for link)

— Denarius Metals DMET DNRSF — The Colombia & Spain mine developer is seeing its shares rise in the wake of a private placement announcement earlier in the week.

I believe the cash-flow/production timeline at Colombia’s Zancudo gold & silver mine is attracting investors. (So is the 25%-plus discount for the Denarius units, with a half warrant. Denarius looks to raise $8.5 million CAD.

As you know (see previous TCRs), I have been to gold-silver Zancudo, and the poly-metallic Spain properties, several times. This, not for forwarding, from CEO Serafino Iacono this morning regarding Zancudo:

[10/21/24, 11:37:19 AM] Fino Colombia Iacono: We should start in two months with 100 tons day 11 gms gold

[10/21/24, 11:37:33 AM] Thom Calandra: with silver correct?

[10/21/24, 11:37:43 AM] Fino Colombia Iacono: 200 gms ton

[10/21/24, 11:38:47 AM] Fino Colombia Iacono: Progressing at 200 tons day and 7 months, plant is ready 1,000 ton day at 8 gms ton gold 140 silver

[10/21/24, 11:39:24 AM] Thom Calandra: 100 TONS OR 1,000?

[10/21/24, 11:40:01 AM] Fino Colombia Iacono: We start with 100 and going to 1,000 end ’25

Denarius is a non-traditional miner. Its shares are listed on the NEO in Canada and over the counter. The company has convertible debentures, high expenses, poly-metallic prospects that could require special treatment and 13% ownership by Colombia’s Aris Mining (El Marmato, etc.).

New Orleans Investment Conference: November 23-25, 2024 — 50th Year

I asked about the steep discount for placement investors. “Yes, stock went up in last 3 weeks and we had price protection and lead orders so we couldn’t change it,” says the CEO-chairman, formerly founder of high-grade producer Gran Colombia Gold.

I do not do private equity placements as a rule. (If our TCR audience can’t get ’em, I won’t chase ’em.) Still, placements offer warrants, discounts and other benefits to professional investors and accredited ones.

I do not own Denarius Metals but once did and made a small profit. Zancudo is for risk-embracers, one that will require airlifting of concentrates from the Colombia mine.

Denarius, Serafino Iacono and team are well known in Colombia and in Spain, and they are controversial for their financings. Yet their community work, hiring, local salaries and benefits for workers at Zancudo and at the Spain properties look to my eye adequate.

The Aguablanca (Spain) property’s nickel-copper concentrates are set to be dealt to a Finland smelter. All told, the Spain properties (Lomero, Toral, Aguablanca) hold gold, copper, platinum, cobalt, lithium. See releases.

— Contango Ore CTGO — The Alaska gold producer (with KinrossGold KGC) is seeing its shares rise $3 to $22 in the past week (NYSE).

CEO Rick Van Nieuwenhuyse tells me he completed a round of investors visits in Europe, NYC and Toronto.

Verbatim: “Just finished a two week road trip through Europe-Geneva-Zurich-Milan then NYC and Toronto. Lots of interest maybe now paying off. Second campaign of processing Manh Choh gold (at KGC’s Fort Knox) about wrapped up with strong free cash flows continued.”

Rick says he expects exploration results on newly acquired Johnson Tract in early November. The shares are trading briskly this week. I own a good amount of Contango and have for several years.

Boilerplate: Annual gold production at Manh Choh is expected to be 225,000 ounces per year with 30% or approximately 67,500 ounces credited to Contango’s account. All-In Sustaining Costs (AISC) are expected be $1,116 per gold-equivalent ounce (with silver).

Trading: I have been adding Aberdeen Platinum Trust PPLT and Ridgeline Minerals RDG, to our holdings. I sold at a loss the remaining Bravo Mining BRVMF we owned.