This is called lining up your future ducks.

Orecap Investment Corp. OCI, a company with a portfolio of miner stakes in pub-cos such as Awale Resources, American Eagle Gold and XXIX Metal Corp., is creating three subsidiaries for future special situations in mining. See release.

“The goal here is to create a series of subsidiaries that will ultimately become new publicly traded vehicles,” a founder and chairman, Stephen Stewart in Toronto, tells me.

Orecap’s Ore Group searches for undervalued mining explorers, thus far in Canada and in Africa. See current portfolio of pub-cos.

“Our deal flow is strong, as is our nose for good opportunities. We want to leverage our people and access to capital to double down on the long-term return of the metals industry – with a focus on Canada.”

When all is said and done, Orecap shareholders will own the new-cos via their ownership of Orecap OCI.

Each will be an independent reporting issuer in the provinces of British Columbia, Alberta and Ontario.

Each subsidiary holds a Free Miner Certificate, allowing it to hold mineral titles in British Columbia.

Stephen tells me the benefit is that the subsidiaries can “independently raise capital.”

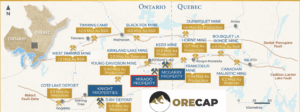

McGarry (Ontario-Quebec) info below.

I own shares of Orecap ORFDF, whose market worth in USD is $13 million. [Orecap does not pay me, with the exception of a single $139 subscription to The Calandra Report.]

Stephen points out that his banking team has developed a process “that allows us to control the entire creation lifecycle from inception to public listing while vertically integrating the process and outcome as much as possible. This gives us control and flexibility to manage the various risks.”

He continues, “They’ll be the next American Eagle AE, the next Awale ARIC. We will own significant equity positions in these new units. We have not been specific on which land packages. Our existing land packages might go into these units but it is likely you will see brand new assets, too.”

Orecap recaps its portfolio companies: here.

Stephen Stewart hired a specialist banker who specialized in private equity for mining for 10 years. “I expect that person to be CEO of one of these assets so we can raise a bunch of capital.”

The McGarry (Kirkland Lake, Ontario) asset is undervalued, ignored, for example, he notes. It is right next to Pierre Lassonde‘s new Gold Candle, a $400 million private company.

“We’re right there, immediately adjacent to Lassonde.” See McGarry video.

McGarry is located east of and immediately adjacent to the Kerr-Addison Mine, producing more than 12 million ounces gold over 58 years ending in 1996.

The pending arrangement, which will require regulatory and British Columbia corporation approvals, and two-thirds of shareholders, “allows us to create new companies and to hold them in the company at the seed level. Orecap gets in at the ground level — at the seed level. It’s a means to an end to create a spinout company.”

Orecap shareholders will own these subsidiaries only through their ownership of the mother ship, Orecap. “I do not believe stock dividends to shareholders create value. You get them one day and sell them the next.”

He adds, “We are going to build value in Orecap and I believe we will have additional value to shareholders.”

Each of these new entities will be structured so that Orecap maintains a “significant” equity position.

Stephen Stewart says he will be co-investing in the new subs personally alongside Orecap.

“These are assets/companies our team sources, vets, finances and builds from the ground up.”

— Thom Calandra

The Calandra Report: Subscribe for $139 yearly via PayPal or credit card

– Option 1 – pay for 1 year here

– Option 2 – PayPal Thom $139 here

Thom Calandra is a writer and an investor. Research and material are meant as editorial opinion. He is not a professional investment adviser. Please do not consider his reporting as a recommendation to buy or sell securities. The Calandra Report, in its 13th year, offers a one-price, $139 yearly fee for all newcomers. Earlier subscribers keep their original cost. Sob stories listened to. No refunds after three weeks of service. Exceptions: groceries, mistaken ambitions.