Shares of EMX Royalty are rising to their highest level in 14 years.

This is the three-year chart:

As reported earlier this week:

EMX Royalty EMX is raising its guidance amid a flood of cash flow. In the reported second quarter, EMX rang up $8.2 million in adjusted royalty revenue. Operating cash flow rose 570% to $9 million. The flow got a boost from deferred payments to EMX by two silver companies. See release.

The company’s shares, with a $345 million USD market value, appear to be attracting investors who are welcoming mining companies with sizable cash-flow gains from a year ago (and even quarter to quarter in the current metals rallies).

The company is reducing debt from a Franco-Nevada credit facility. See details. It had approx. $25 million of debt and $17 million of cash on its books as of the completed June quarter. Working capital surplus: $30.1 million.

The company set its guidance boost for 2025 to adjusted royalty revenue of $30 million to $35 million. “The noted increase in expected adjusted royalty revenue compared to the original guidance is due to the significant increases in metal prices to date in 2025,” EMX says.

Previous guidance was $26 million to $32 million. Revenue includes option and property payments.

Dave Cole is EMX CEO. “Too undervalued for too long,” Dave texted me just now.

Source: EMX Royalty

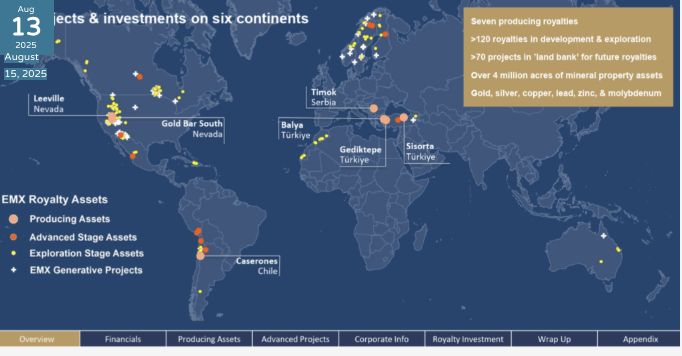

EMX has a broad package of metals royalties (gold, silver, copper, molybdenum, zinc, lead) on six continents. Net smelter returns in Chile, Serbia, Nevada and Turkey are actively contributing to revenue.

The Colorado-based company is buying back shares at a clip of approx. 5 million a year. Its average price for the EMX purchases was $1.65 USD in 2024. The stock today is $3.30 at last look.

Source: EMX Royalty

See the current EMX investor presentation here.

I own shares of EMX and have, on and off, for eight or 10 years. My other significant roy-co holding is Elemental-Altus Royalties ELE ELEMF.

ELEMENTAL-ALTUS recently saw stable-coin company Tether purchase ELE shares for investment purposes.

Aside from stable coin operators that could widen their ownership of commodities, perhaps in coming months we will see more investment firms, private equity, endowments and non-specialized funds, even international theme mutual funds, start buying into roy-cos and metala miners with global geographics.

That’s something to chew on.

— Thom Calandra

The Calandra Report: Subscribe for $139

– Option 1 – pay for 1 year here

– Option 2 – PayPal Thom $139 here

Thom Calandra is a writer and an investor. Research and material are meant as editorial opinion. He is not a professional investment adviser. Please do not consider his reporting as a recommendation to buy or sell securities. The Calandra Report, in its 13th year, offers a one-price, $139 yearly fee for all newcomers. Earlier subscribers keep their original cost. Sob stories listened to. No refunds after three weeks of service. Exceptions: