Ivanhoe’s Platreef To Develop Into ‘Godzilla’

Ivanhoe Mines‘ Platreef volley is fresh on the wires. See the ‘super-giant’ release.

South Africa’s Platreef platinum (gold, nickel, copper, etc.) complex, via Robert Friedland‘s Ivanplats in 2003, was my second introduction to Ivanhoe. Mongolia’s Oyu Tolgoi copper-gold project in the Gobi was my first.

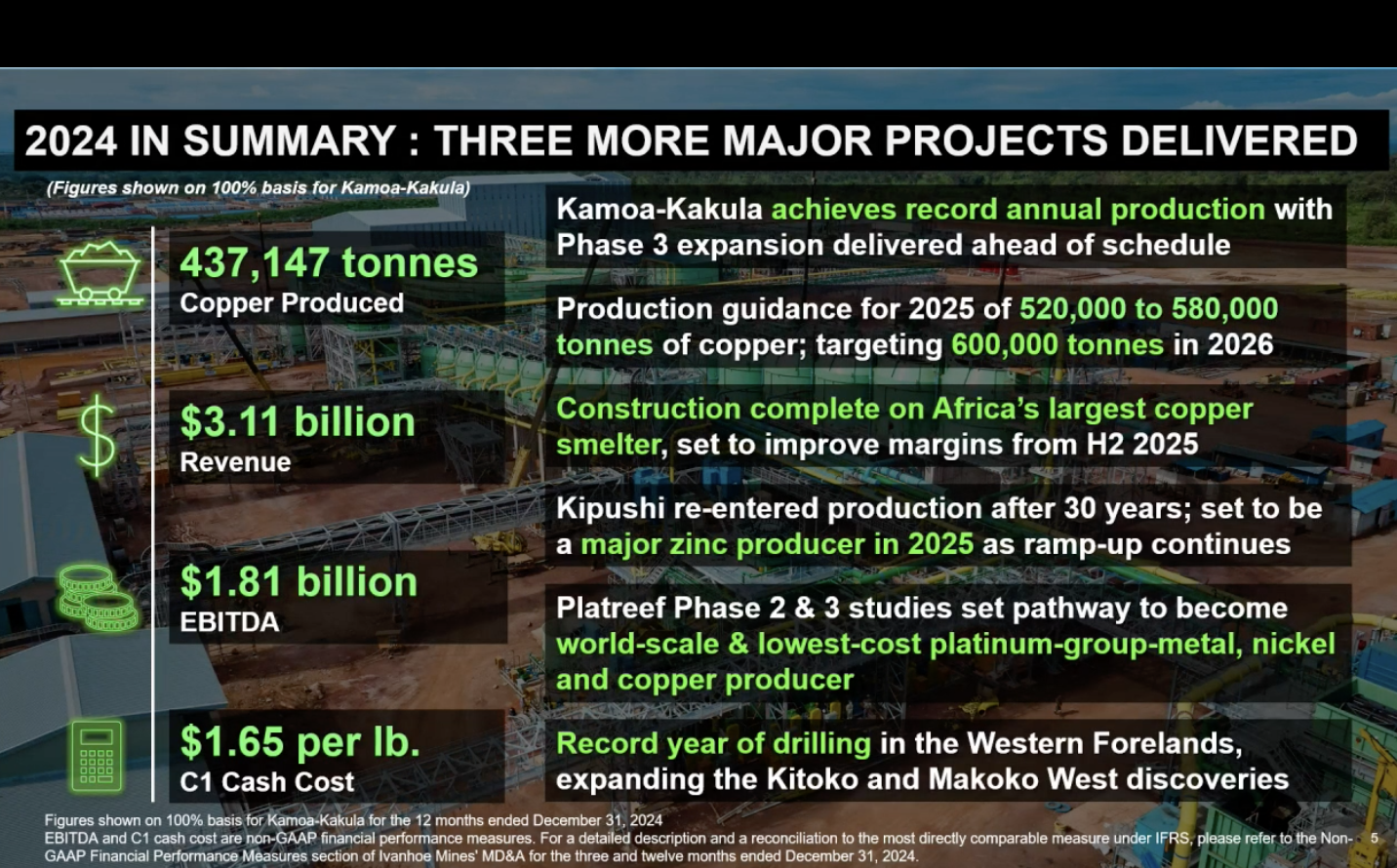

Q4 and 2024-Year Ivanhoe Numbers: Records For Revenue ($3.11 Billion), KAMOA-KAKULA Copper Output

Also below:

- Alamos Gold Notches New High *

- Banyan Gold Raising Its Yukon Grades **

- TRADING NOTE

On that broiling South Africa day, I was late to the party: Platreef’s Ivanplats property was in the miner’s portfolio bag six years before I got there.

Granted, MAGNIFIED language, such as “Godzilla of a mine,” is order of the day for the Ivanhoe Mines chief.

Being fair, I point out that Robert Friedland has always stayed true to his school with this property on the Northern Limb of the rich Bushveld complex.

“Biggest … lowest-cost … most technologically advanced … richest … generations of output, jobs, mineral supply chains” — all consistently stated for the thick layers of platinum-group metals beneath the Northern Limb.

He was “consistent” in 2003, when he — in black tie and like all of us pale folks, sweating rivers of salt out of our bodies — introduced me to the sprawling property at Mokopane.

The release just out is an expansion study of Platreef timelines, costs, accelerated phase developments and billion-dollar NPVs (net present values). Ivanhoe pledges on a global scale to be:

“The lowest cost platinum, palladium, rhodium, and gold producer; with significant nickel and copper.”

Early phases, starting toward the close of this year of 2025, will show an annualized pace of 450,000 ounces (so-called 3(P)E platinum group metals + gold, if I understand the terminology correctly). Two or so years on from that: a yearly pace of 1 million ounces of platinum, palladium, rhodium and gold, plus 25,000 metric tons of nickel and 15,000 tons of copper — a metal, along with zinc, that Ivanhoe mines in size in the Congo Copper Belt.

Re: Ivanhoe Mines‘ amagnified text, graphics and direct quotes — It is all here. The company in its several iterations, going back to 1996, has always made investors money.

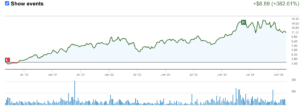

Still, investors at first were lukewarm Thursday after Q4 and year-end numbers and a conference call. See report. After a detailed conference call, the shares were back on track, rising 2%.

Inconsistent power grid flow at Kamoa-Kakula, and a provisional tax charge that reduced operating cash flow, are likely reasons for IVN IVPAF shares’ drop at first Thursday. Explanations by Ivanhoe CEO Marna Cloete and other execs provided clarity that investors seemed to heed. (I know I did.)

I bought into Ivanplats when it was private in 2003 and still hold many of those now-public IVN IVPAF shares. (Approx, 78,000 shares owned, and one hour or so ahead of Ivanhoe Mines’ Q4 financials, which will tick off DRC Congo’s profitable Kamoa-Kakula copper and Kipushi zinc mine, I added $3,100 worth at the current, what I see as well-below-fair-value price of $11.25 USD.

A day later, amidst that conference call Thursday 8:30 a.m. PT, I bought another $2,000 worth at $10.99.)

“Ivanhoe has always grown through exploration,” Robert Friedland said today on the conference call. He detailed new copper and silver-bearing trends in Kazakhstan. Conference call link here.

Also: further intensive exploration at Western Forelands in DRC Congo.

That is enough for now. Except to say that when I last emailed with the Ivanhoe chief three days ago, I told him I expected an all-time high for the IVN stock this week. Premature? Looks so. I am still buying below $11 USD as of Thursday Feb 20 2025.

As for the independent studies that detail three phases of Platreef mine, once again: ’tis all here.

Platreef is probably on track (I am not including outer-space mining) to rank as a Top 3 undeveloped precious metals deposit: 56 million ounces of platinum-equivalent indicated (category) mineral resource and another 74 million inferred. That is with a 2.0 grams per ton and a 3(P)E+gold cut-off.

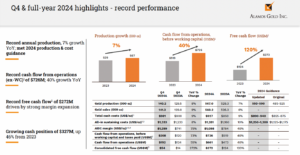

- *Alamos Gold: record gold production AGI — Q4 and year end here. And here. Stock hits all-time high; I own AGI. Slide from deck just below. Boilerplate: Produced 567,000 ounces of gold across its Canada and Mexico mines in 2024, a 7% increase from 2023.In addition to Alamos Gold, when it comes to monthly stock performance, shares of Avino Silver & Gold ASM, a Mexico producer, are up 34% from January 24 to today.

- ** Banyan Gold BYN also is up almost the same one-month amount as Avino. Tara Christie at the Yukon developer is delivering on pledges to raise gold grades at AurMac’s Power Strip tar9gets. These hits are showing respectable economic stretches there on the eastern end of the deposit — ones that will factor in when Banyan weighs in with its first eco-appraisal later this year. I do not own Avino; I bought more Banyan Thursday at 18 cents USD. BYN assays here.

- Trading note: SELLING the rest of shipper DHT Maritime DHT-NYSE at break-even. SHIPPING LANES, tariffs, oil prices, lease rates are all in great flux. … Sold half of GHANA developer Newcore Gold NCAU at a profit; waiting to see next steps for the Enchi Project. … Considering selling the rest of deflated Alaska developer and joint venture miner Contango Ore CTGO-NYSE at a loss after many profitable holds and sales the past 3 1/2 years. … Selling $1,200 USD worth (approx.) of rapid gainer Integra Gold ITRG-NYSE; we will own approx. $13,000 worth after the sale.

Entire The Calandra Report here.

— Thom Calandra

Thom Calandra is a writer and an investor. Research and material are meant as editorial opinion. He is not a professional investment adviser. Please do not consider his reporting as a recommendation to buy or sell securities. The Calandra Report, in its 13th year, offers a one-price, $139 yearly fee for all newcomers. Earlier subscribers keep their original cost. Sob stories listened to. No refunds after three weeks of service. Exceptions: