Remember when the trade organization Denver Gold Group held its annual Americas Forum in, where else, downtown Denver?

The not-for-profit member group of miners packed its bags to Colorado Springs years later.

In the early 2000s, as a wire service reporter, I ventured to downtown Denver for the show a few times. This was when we were developing MarketWatch.com.

Mining Forum Live is a free newsletter that the Denver Gold Group is forming. I have to mention that Denver Gold Group does not pay me for this report; neither does any other executive or group or company. I do this to put ordinary investors, individuals, on good ground for what I think will be a runaway interest in miners and their stocks and convertibles and placements and other investment vehicles. — Thom Calandra

Timothy Wood of Denver Gold Group

Back then, 20 and 25 years ago, I had to plead to the group for a press pass; sometimes I was successful and sometimes I was not.

The hotel setting in downtown Denver was blah, musty — yet the presentations were mostly top notch; most of them staged by heavyweight miners.

The streets back then, say 20 years ago? At night, crime rates downtown and on Capitol Hill soared.

Little has changed. Assaults causing serious bodily injury appear to have doubled since 2012. The FBI says the violent crime citywide shows “the fastest rate of growth of any city with more than half a million residents.” Denver Police report approx. 4,900 aggravated assaults a year, up from 2,460 in 2012.

Still, some of the “extra-curricular” evening activity, I recall, was a hoot: a few roasts, a burlesque variety show, plentiful steakhouse dinners staged by deep-pocket miners. A hoot — as long as you survived the walk to the theater, or the restaurant, that is.

At the show itself, well, these were the days when pub-cos, not just miners, concluded their public presentations with a BANKERS ONLY informational session behind closed doors.

Once, I somehow slipped into I believe it was a Newmont Mining presentation, but it could have been another top-tier miner. I reflected some of the executive comments without direct-quoting anyone and caught all heck for it from IR/PR representatives.

In those days, downtown Denver was, let’s say, dicey. “Downtown Denver is unpleasant, uninhabitable, and uninvestable – desperate to beat San Francisco in a race to the bottom, Timothy Wood, the DGG‘s executive director since 2011.

(I will beg to differ about SF — still, perception is 70% of the challenge for what I call “suffering city” syndrome.)

Wood as a South African mining journalist was at the top of his reporting skills, logging scoops for newspapers, magazines and web sites in his native land. He also assembled several software and conference companies and co-founded JSE-listed (at the time) Moneyweb, and its Mineweb. Also ResourceInvestor.com.

I met Tim through Sandy Lawrence, a delightful and early pioneer who was running International Investment Conferences: the go-to mining show operator in the mid-1990s through mid-2000s. Tim’s ResourceInvestor.com merged with Sandy’s group in 2003, and I met Tim at the annual SF Gold Show, which I had been attending as an SF newspaper reporter for years.

I set out with this “conference” piece to give anyone interested in the mining sphere a topical look at mining shows. Specifically, how an investment conference, and there are way too many to catalogue, introduces investors both individual and professional to the arcane segment of metals.

My focus here, trade organization Denver Gold Group, by its charter represents the largest miners, and recently smaller ones, as an independent entity. At present, it has 157 dues-paying members.

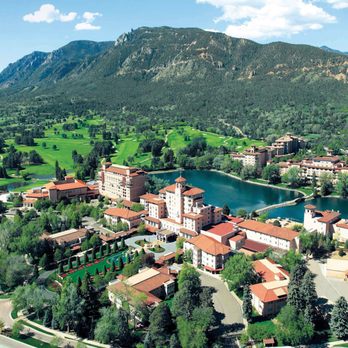

Denver Gold Group’s operation these days is in Colorado Springs, and in Zurich (April). The Americas Forum takes place each September at The Broadmoor. The five-star hotel is more like a city set among serious mountains, valleys and streams.

Layout of The Broadmoor in Colorado Springs

The members currently include the big miners, the mid-tier ones and even a small-co miner or three. Most are public.

By stating its criteria for membership, and show appearances, DGG tries to set itself apart from conferences that include any company in exchange for exhibit fees. The benchmarks:

Must be within 15 months of first production.

Market capitalization must be 25% or more of metals reserves.

Other precious metals are converted to gold equivalents.

Other considerations include coverage by a recognized bank; a primary mineral such as gold, silver, platinum, palladium and diamonds and others. These commodities must make up 60% or more of actual or projected consolidated revenue. See: https://www.denvergold.org/membership/

The action for mining conferences these days is led by operators who have entirely embraced software, Internet marketing, tele-conferencing and … well, the best food, settings, resorts and staffs. Plus: superior speakers, emcees, organizational skills, one-on-one meetings and so on.

The five best known and longest-standing show operators on this side of the world are Denver Gold Group; Precious Metals Summit(also with its marquee show in Colorado at Beaver Creek); New Orleans Investment Conference(in its 50th year and held in November); Toronto’s massive Prospectors Developers PDAC (each March — 25,000 attendees) and, as is Denver Gold Group, a not-for-profit and independent trade organization; and the also independent and geology-focused trade group AME British Columbiaand its 300-company Round-Up in January.

Naturally, some operators will take my head off for not including their North America shows or offshoots. Leave it said, perhaps three or four of these shows are successful, specialized and draw hundreds of moneyed attendees and bankers who sell out the events.

I will let Tim tick off the evolving business of investing in mining; it is worth a 2-minute scan.

Over the 36 years of our platform, the capital markets for mining have undergone an incredible sea change. London has become much less competitive as a center of mining capital formation, especially for juniors. — Tim Wood, Denver Gold Group

Other points that might help new investors fathom the intertwining of mining and capital markets (read: available investors’ money).

— Johannesburg, once a leader for funding and mining exposure, is “dying off rapidly,” Tim Wood notes.

— Toronto is more dominant thanks to its mining friendly jurisdictions (flow through, permitting, labor pools, etc.), competitive governance (National Instrument 43-101) and credible banks.

— Australia now eclipses South Africa capital origination, project activity and investability: 26 companies with primary listing and projects down under worth $40 billion USD. That is fourth behind Canada ($119bn), U.S. ($100bn) and China ($63bn).

— Sell-side (banking) has radically changed for mining. Much less research coverage.

— Hedge funds, private equity and family offices have achieved a dominant market share among investors over the last decade.

— Juniors are dependent on “business development” funding from senior companies, and the traditional equity pipeline is much less viable.

— Gold equity premium (shares vs. physical metal) has been crushed since the 2004 peak.

— M&A has driven an unprecedented rate of consolidation the past five years

“The industry is shrinking and becoming much more disciplined with the money and projects available to it,” Tim said.

I look to weigh in from the show in September.

My signature Colorado Springs moment came a couple of years ago. Ivanhoe Mines‘ Robert Friedland, a successful mine builder in Africa and in Mongolia, started his keynote by describing the industry as “the dumbest business in the world,” and I paraphrase.